Analogies v.3 — what do VCs, book publishers and movie producers have in common — cut losses, double down on winners

VC investment business model is similar to the book publishing and movie industries — it is dominated by betting on “blockbusters” and the power law. A few stars in the portfolio will create the vast majority of your returns, while the rest of the portfolio loses money. This is why all of these industries focus investments on their winners and add more follow-on investments to those that show signs of becoming blockbusters, while cutting their losses on all other investments.

Book publishing — follow-on investments double down on winners

American publishing industry invests into publishing approximately 1 million titles per year. An average book sells about 300 copies per year and under 1000 per lifetime. If you want to be ranked as a “best seller” you have sell more than 5,000 copies. Only about 2% of all the published books manage to become “best sellers.” Publishers lose money on the vast majority (ca 90%) of the books that come out every year. A recent court case brought to light that of all the books Penguin Random House publishes “just 4 percent — account for 60 percent of … profits.”

Only 300 books (0.0003% of all published books) per year sell over 100,000 copies and cover the losses from publishing all the other books. About 10 books out of the million published per year pass the 1 million copies sales mark. Finding and keeping outliers like Danielle Steel, Dean Koontz, Stephen King, Paulo Coelho, and John Grisham is key for success in the publishing industry's business model.

With this business model the publishers have to get the most out of the potential blockbusters, so follow-on investments into marketing and advertising go to those that show success in pre-sales or in first week of sales.

Follow-on investments by publishers are very conservative: tier-one sellers (“best-sellers”) get about $25,000 per title, while tier-two (“mid-list”) get from $10,000 to $20,000, and the bottom third of the authors often get nothing. However, one or two blockbuster titles will get massive financial support from the publisher to make them even more successful — getting from six to seven figure investments for marketing, advertising, travel and publicity to further drive sales of these “blockbusters.”

Movie production — follow-on investments double down on winners

Movie industry is famous for its efforts at avoiding payment of royalties, lack of financial transparency and the “Hollywood Accounting” practices (quite similar to professional sports teams). However, the “blockbuster” investment strategy clearly prevails in the movie industry as well.

Author Anita Elberse in her book Blockbusters: Hit-making, Risk-taking, and the Big Business of Entertainment summarizes the movie industry investment strategy:

“Smart executives bet heavily on a few likely winners. That’s where the big payoffs come from.”

Approximately 500 movies are released per year in American movie theaters. About half of these are Hollywood studio (big five) productions, the rest are independent productions.

Independent movie production accounts for 95% of all movies made in America every year, but the vast majority of independent films never get released in movie theaters. Only 3.4% of independent films made a profit while “nine out of ten didn’t get a theatrical release” and were unlikely to make back their full investment.

Most Hollywood movies also lose money. The number that has been mentioned by several Hollywood insiders is — 80% of all Hollywood movies lose money and 60% of those that are released in theaters lose money. WIth this business model the studios are locked into a strategy of “making disproportionately big investments in a few products designed to appeal to mass audiences.” The movie industry operates in a world of many losses, some break evens, and a tiny number of huge “blockbuster” hits that make all the money for the studios. As Imax CEO Rich Gelfond explained to the The Hollywood Reporter:

“A trend that will accelerate is blockbusterization … There will be a lot more blockbusters than mid-range movies.”

For big budget movies Hollywood doubles down and invests an extra 50%-80% on top of the production cost to promote and market the movie in North America. For the top summer blockbusters studios will set aside 100% of the production cost for investments into marketing (extra $150 million investment), while “mid-budget” movies with sub-$60M production budgets (most of the movies made) are lucky to get 15% (ca $10M) investment for marketing. The follow-on investment strategy for Hollywood is clearly:

Smaller titles, mid-budget films, artistic/creative films, and adult-audience targeting dramas largely fail to provide a sufficient return on investment. This is why we keep seeing studios release and heavily promote sequel, prequel, spin-off, or reboot movies.

Venture Capital — follow-on investments double down on winners

When talking to potential portfolio startups VCs talk about the size of the average ticket and often hasten to add that they reserve “as much or more” money for future follow-on investments. This is true — on paper VC funds set aside about 40%-60% of their funds for follow-on investments.

As such, founders can be forgiven for thinking that the VC will continue to invest in them in future rounds come rain-or-shine. However, often it comes as a devastating surprise when VCs decline to invest in bridge-rounds, use their pro-rata investment rights, or lead the next round of financing. The generally unspoken and uncomfortable reality is that the follow-on money is not reserved equally for everyone, but is focused mainly on the few perceived “winners” of the portfolio.

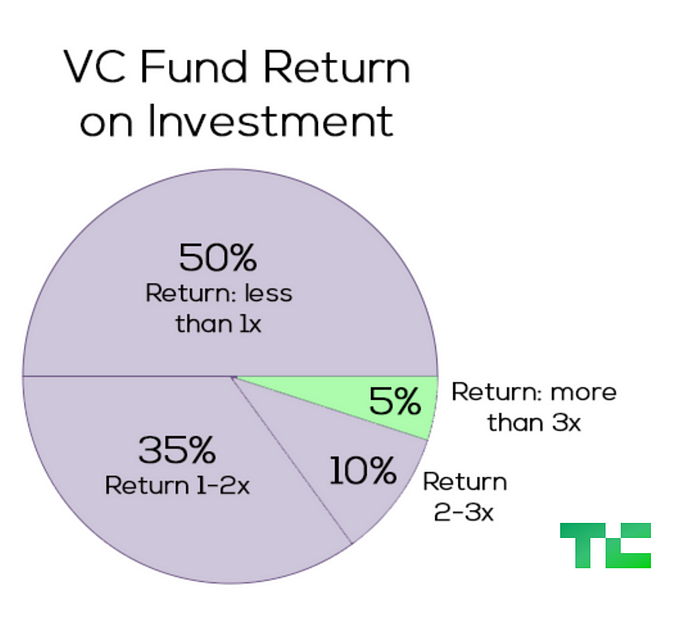

To understand this logic it is important to remember that “Pareto Principle” and “power law” dominate the VC portfolio math. Statistics over the past 40 years of VC investing show that approximately 50% of an average portfolio gets written off. This means that one or two startup exits (about 5% of portfolio) will have to pay for all the investments, write-offs, all the costs and fees, and generate all the profits for the whole fund.

See also:

https://taschalabs.com/why-you-dont-want-to-be-a-venture-capitalist/

A winning strategy for VCs is therefore putting big money bets on likely “blockbuster” winners, and not in the 0, 1 and 2X returners. Therefore, when VCs have to make follow-on investment decisions, they look to concentrate the most capital in a select few top companies (potential “fund returners” that are the most likely to reach unicorn valuations) in the portfolio so as to reduce dilution of their shareholding in these predicted winners.

Something to consider by VCs and founders is that this strategy can potentially have some dire effects on the startups that are not the portfolio leaders. There is a potential “signalling risk” (optics effect from the insider VC not participating) being sent to next round investors (outside VCs may assume that the insider knows something they don’t and avoid investing). An insider VCs decision not to invest could make fundraising even harder for the founders. At the same time it is not entirely clear whether “signalling risk” plays a decisive role for new VC investors or whether there are other reasons for failing to raise the round. One study of 30 US startup rounds showed no significant effect from failure to follow-on invest concluding:

“ good investors are trying to find the best companies and entrepreneurs to get in business with based on the evidence of the business as opposed to making decisions based on perceived signaling factors”

The “blockbuster” or “winner-take-all” model of VC investing probably explains why portfolio startups that need the most help in scaling sales (slowest to grow), and those that are having difficulties in finding next round’s funding (perceived as difficult or unattractive projects) will get a “No” from most of their VCs, while a startup that has lots of term sheets will see their VCs trying to not only fill their pro-rata, but also fight to put extra money into the company. As such, startup founders should not just assume that their VCs are locked-in and will automatically invest in their next round.

My advice to getting follow-on investments:

select VCs wisely to avoid “fairweather friends,”

keep the VC in the loop through frequent updates of all your successes,

paint the path to being a future “fund returner” for the VC — especially if the current results are lagging your pitch deck promises.